Advisors Speak Out on Inflation, Midterm Elections, Future of Work and More

June 17, 2022

The first half of 2022 has been tumultuous, rocked by Russia’s invasion of Ukraine earlier in the year, which only exasperated inflationary pressures and long-simmering supply chain issues. Add it all together, and it’s no surprise that stocks have taken a nosedive.

Against this backdrop, we recently checked in with our financial advisor members to assess their outlook on various issues, including the economy, potential challenges they face in their business and the upcoming midterm elections. We collected 459 responses from May 15–27. The results reflect an industry that is cautiously alert and optimistic about the future. Here’s a closer look:

With prices on everything from groceries to gas to clothing rising at the fastest pace in more than four decades, the Fed has raised rates multiple times this year. This, however, could be just the beginning of the central bank’s tightening cycle. Many experts contend that at least two more hikes are in store for 2022.

Nonetheless, most respondents were optimistic that the worst is behind us, with 44% saying inflation will flatten out during the rest of 2022. On the flip side, more than a third of the respondents (37%) predicted that inflation would continue to rise, while about 19% said it would decrease.

Stocks have endured one of the worst stretches in recent memory. The S&P 500 was down about 14% through the end of May. The tech-heavy NASDAQ – which includes so many of the pandemic darlings like Netflix and Peloton – fared even worse, off by 24% during the same period.

Still, optimism reigned supreme among survey respondents. Nearly 45% said they believe equities will rebound and get stronger to finish out the year. One-third thought the markets would flatten out from here, while 22% said more losses are in store.

Almost overnight, the pandemic changed how people worked. As with nearly every other profession, the initial outbreak forced financial advisors to stay home and use digital platforms like Slack, Zoom and Teams to conduct client and other business meetings. But as Covid-related restrictions have eased, another shift is underway – at least according to our survey.

Indeed, more than 75% of the respondents indicated that most or all their client meetings are now in-person. Twenty-three percent are mostly virtual, while fewer than 2% have eschewed face-to-face meetings altogether.

Most political pundits expect Democrats to struggle in the upcoming midterm elections. After all, the president’s party tends always to lose seats in Congress in off-year elections. That’s the way our members see it as well.

About 74% of the survey participants expect Republicans to wrestle control of Congress. Few than 4% said the Democrats would have power, and 22% believed there would be a split.

Despite the breakneck pace of consolidation in the financial services industry, survey participants don’t expect to engage in M&A or succession planning to expand their businesses. Only 7% said that path would drive their future growth.

Instead, referrals ranked at the top, with 55% saying they would be a key growth opportunity. Organic growth accounted for 17% of the responses and proactive prospecting represented 12%. Next-gen clients, new technologies, offering more ESG-themed investments and DEI initiatives made up the rest of the responses.

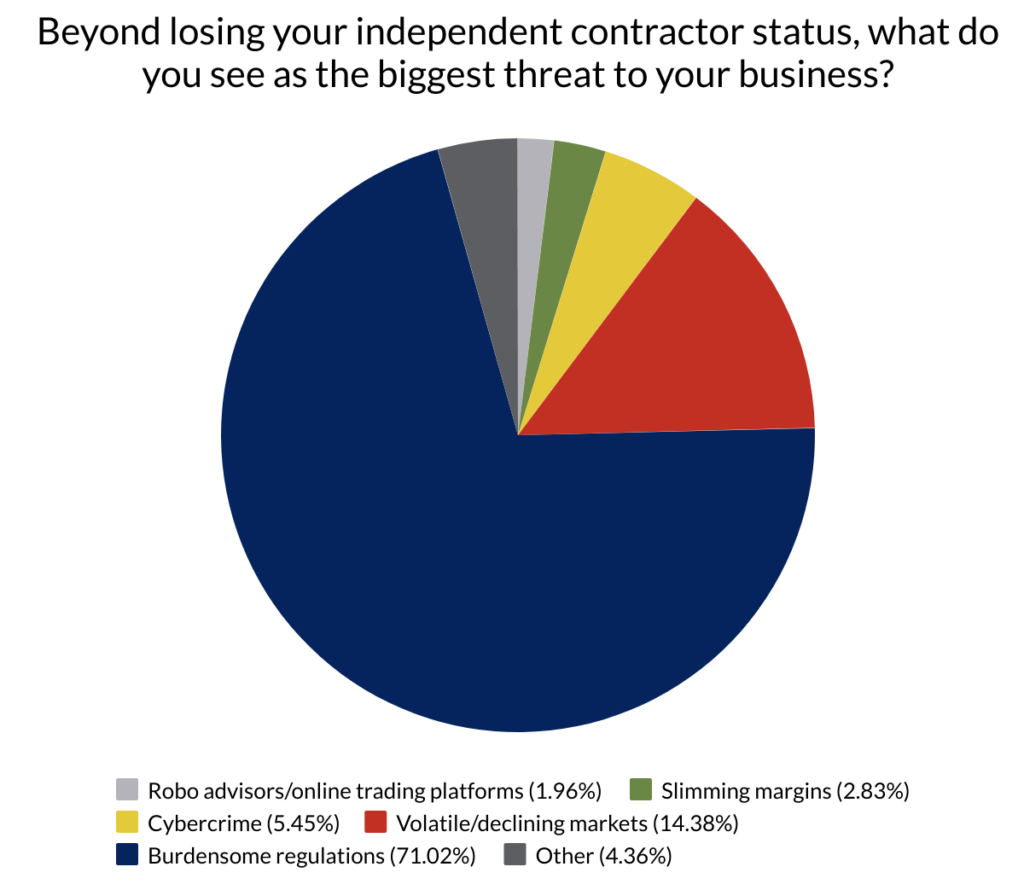

Independent advisors losing their independent contractor status is an existential issue for our members. That much is clear. But beyond that, we asked respondents what other potential threats to their business most concerned them.

An overwhelming majority of the respondents (77%) cited burdensome regulations. Volatile and declining markets ranked second with 14%. Other threats included cybercrime, slimming margins and robo advisors/online trading but made up a small percentage of the responses.